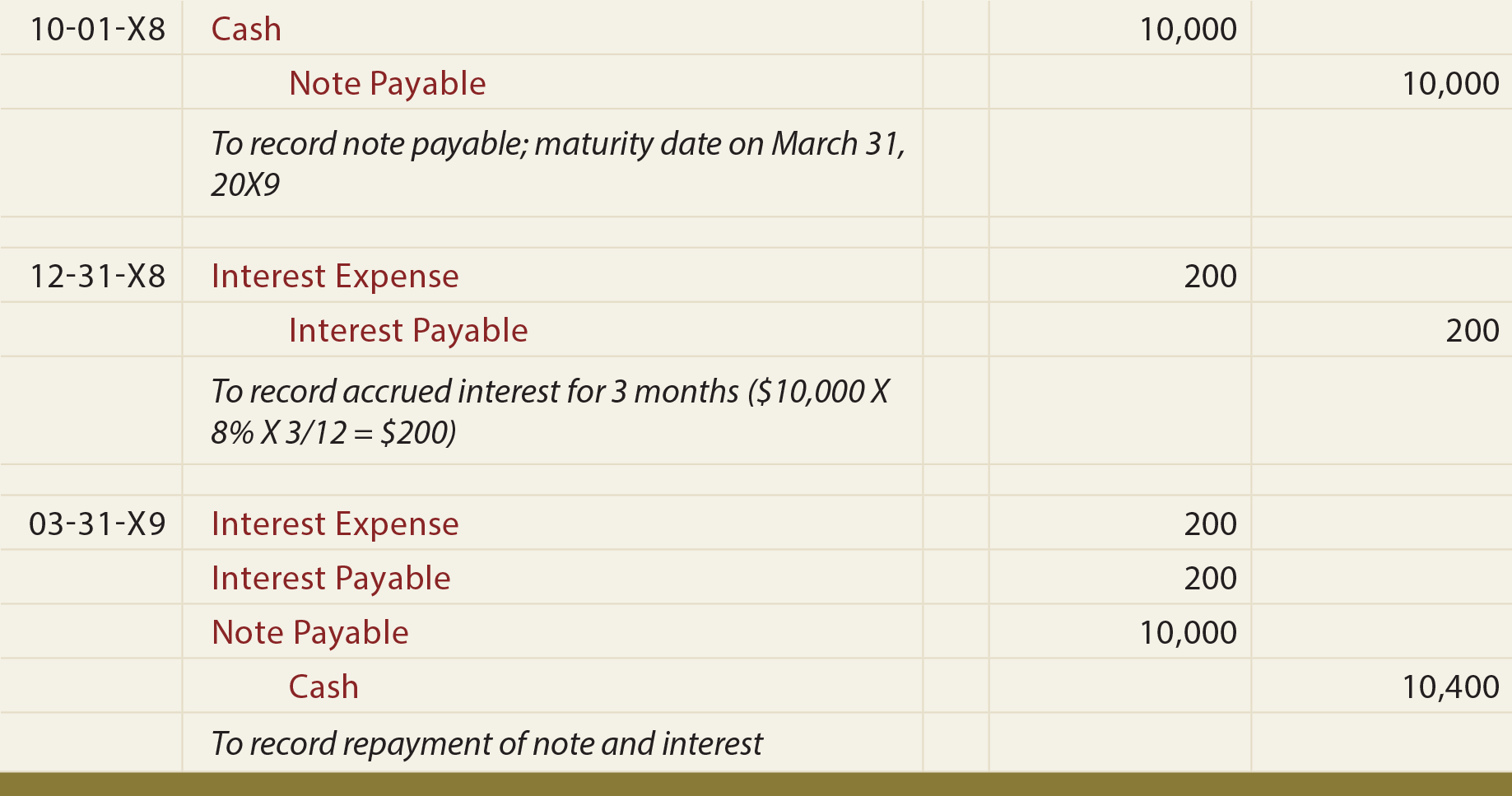

Periodic interest accrued is recorded in Interest Revenue and Interest Receivable. The following example uses months but the calculation could also be based on a 365-day year. Notes receivable have several defining characteristics that include principal, length of contract terms, and interest. The principal of a note is the initial loan amount, not including interest, requested by the customer. If a customer approaches a lender, requesting $2,000, this amount is the principal. The date on which the security agreement is initially established is the issue date.

Do you own a business?

It is possible to combine the previous two entries by debiting Notes Receivable and crediting Sales. Together, the principal and interest portions represent the note’s maturity value. In some industries, it is common for a seller to insist on a note rather than an open account for certain types of sales.

Notes Receivable Terms

Upon approval, the $7,000 is deposited into the business’s checking account the next day and then Square charges 9% of the business’s credit card sales each day until the $7,910 is fully paid. Square says that the advantage of this percentage-of-sales method is that the business does not have to make large payments when business is slow. The percentage that Square charges stays constant until the loan is paid off fully. On 1 May 20X4, PQR, Inc. lent $2 million to ABC, LLC for 2 years against a documented promissory note. DEF, Inc., another client of PQR, Inc. issued a 2-month promissory note against their outstanding balance of $3 million on 1 November 20X4.

- If a customer approaches a lender, requesting $2,000, this amount is the principal.

- If it is a compound interest, the accrued interest that remains unpaid is added to the principal of note receivable and carried over to the next accounting period.

- This results in a reduction in the principal amount owing upon which the interest is calculated.

- Notes receivable are financial assets of a business which arise when other parties make a documented promise to pay a certain sum on demand or on a specific date.

- For the purposes of accounting class, we will focus on Accounts Receivable transactions where an Accounts Receivable is turned into a Note Receivable.

Create a Free Account and Ask Any Financial Question

This is treated as an asset by the holder of the note, and a liability by the borrower. Overdue accounts receivable are sometimes converted into notes receivable, thereby giving the debtor more time to pay, while also sometimes including a personal guarantee by the owner of the debtor entity. The guarantee provision makes the note receivable easier to collect than a standard account receivable. When a note receivable originates from an overdue receivable, the payment tends to be relatively short – typically less than one year. To illustrate notes receivable scenarios, let’s return to Billie’s Watercraft Warehouse (BWW) as the example. BWW has a customer, Waterways Corporation, that tends to have larger purchases that require an extended payment period.

Part 2: Your Current Nest Egg

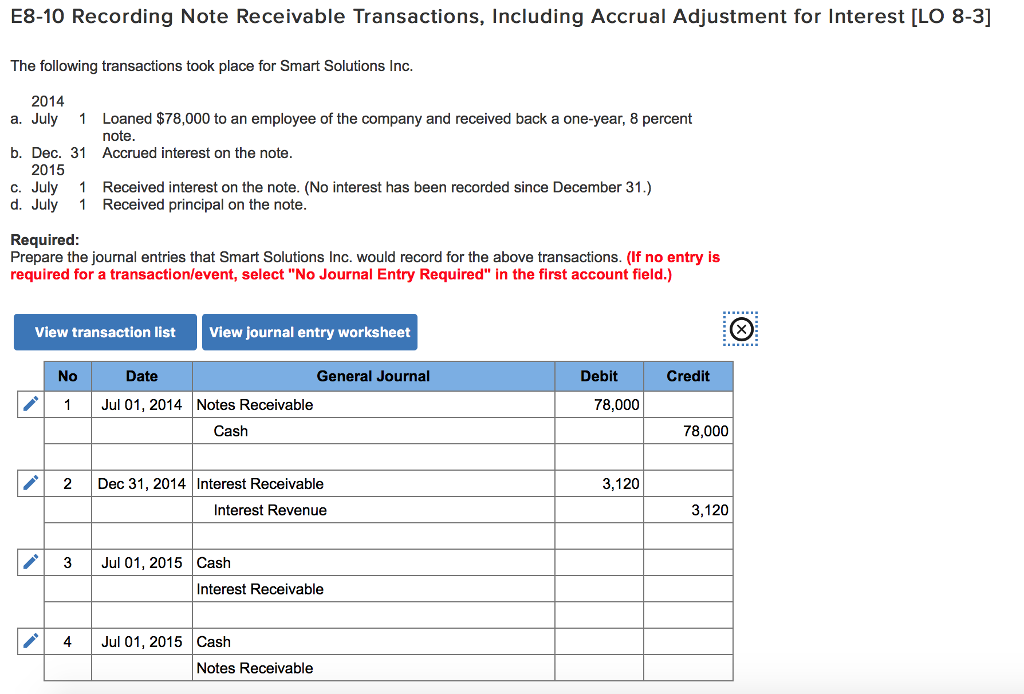

Rather than using Interest Receivable for the one day of interest in April, we record it as part of the cash payment, skipping the step of first entering it in the receivable. Accounts Receivable is a normal business transaction for between a company and its customer. The intent is for the debt to be settled in the normal course of business, usually in 30 days (depending on the terms of the account.) It typically does not have an interest rate. (a)”One year after date, I promise to pay…” When the maturity is expressed in years, the note matures on the same day of the same month as the date of the note in the year of maturity. As at 31 December, the note receivable from ABC is classified as a non-current asset because it is due after 12 months from 31 December. Interest receivable on the note as a 31 December is reported as current asset because it is to be received at the end of April 20X5.

Note receivable from ABC LLC carried 5% simple interest rate payable annually while the one from DEF Inc. carried 8% interest compounded monthly. Just as was the case with accounts receivable, there is a possibility that the holder of the note receivable will not be able to collect some or all of the amounts owing. When the investment in a note receivable becomes impaired for any reason, the receivable is re-measured at the present value of the application form currently expected cash flows at the loan’s original effective interest rate. At month-end adjusting entry, the company can make the journal entry to increase the balance of the note receivable by debiting the note receivable with the amount of present value multiplying with the discount rate. Interest revenue from year one had already been recorded in 2018, but the interest revenue from 2019 is not recorded until the end of the note term.

A note’s maturity date is the date at which the principal and interest become due and payable. For example, when the previously mentioned customer requested the $2,000 loan on January 1, 2018, terms of repayment included a maturity date of 24 months. This means that the loan will mature in two years, and the principal and interest are due at that time. The following journal entries occur at the note’s established start date. Notes receivables are written promissory notes which give the holder or bearer the right to receive the amount mentioned in the agreement. Sometimes accounts receivables are converted into notes receivables to allow the debtors to pay the balance.

The present value of a note receivable is therefore the amount that you would need to deposit today, at a given rate of interest, which will result in a specified future amount at maturity. The cash flow is discounted to a lesser sum that eliminates the interest component—hence the term discounted cash flow. The future amount can be a single payment at the date of maturity or a series of payments over future time periods or some combination of both. However, for any receivables due in less than one year, this interest income component is usually insignificant.

Also, the company may be able to sell the note to a bank or other financial institution. When a customer does not pay an account receivable that is due, the company may insist that the customer gives a note in place of the account receivable. BWW issued Sea Ferries a note in the amount of $100,000 on January 1, 2018, with a maturity date of six months, at a 10% annual interest rate. On July 2, BWW determined that Sea Ferries dishonored its note and recorded the following entry to convert this debt into accounts receivable. Cash or bank is debited by the sum of principal amount and interest not yet received.